Why startups fail? For more top-down thinking

Why do startups fail outright, or fail to reach the skies? I argue that a lot has to do with too *little* top down thinking in picking a good product/market combination to begin with

The other day I was scrolling X and saw the following post:

It got me thinking.

The first thing that came to me is that ~all startups fail (i.e., go out of business) because of a lack of product-market fit. When there is real product-market fit, all problems are solvable, because maintaining strong growth tends to feel *more* like chasing a boulder down the hill; maintaining growth with weak PMF (or lack thereof), on the other hand, feels *more* like pushing said boulder up the hill.

If we take “fail” in a more latu sensu, why so many startups fail to be huge success stories, such as unicorns, decacorns, etc., when they've survived that first stage with some form of PMF? Probably because they picked a small market, or a big market with terrible dynamics (airlines, anyone?).

In any way, where that thinking got me to is that so much of the success of a startup is a function of the product/market that founders decide to tackle. And to get back to the initial tweet, there's not a lot of content out there on how to pick a good market.

Moreover, most content about the earliest stages of the startup journey tend to be somewhat misleading.

Most founding stories, on the one hand, tend to romanticize how founders first get to pick their ideas (and that's understandable, bc these stories are geared toward current/prospective customers and employees, not other founders). David Velez, founder of Nubank, tells the story of how he decided to work on Nubank after being stuck in an armored revolving door when struggling to open his checking account in a bank branch. That moment might have had an impact on the trajectory, but truth be told, David was a highly sophisticated founder, keenly aware of the ingredients of Silicon Valley-type successes. He had worked both at General Atlantic, a famed tech growth investing firm, and Sequoia, which needs no intro. He had scoured Latam in search of venture-scale businesses to invest in on behalf of Sequoia, frequently in the company of Doug Leone, the legendary Sequoia managing partner. If there is one founder that was well-informed on what it took to make it big, it was him. That explains why he picked an industry that was incredibly large in Brazil - banking - with an oligopoly of a few tech-backwards banks that were stupidly profitable. Or why he picked an industry where customers were being treated poorly, and had to jump through whoops to go over internal limitations of these oligopolists, such as their inability to open up a checking account without having the poor customer go over to a bank branch. Or why he picked an industry regulated by an vanguardist Central Bank that was giving lot's of indications that it wanted more competition. In other words, David thought A LOT about what and where to start up.

Most founding advice, on the other hand, tend to downplay the role of picking a good starting point, or being very judicious about where to pivot to. Paul Graham, for example, says about finding out How to Do Great Work:

The first step is to decide what to work on. The work you choose needs to have three qualities: it has to be something you have a natural aptitude for, that you have a deep interest in, and that offers scope to do great work.

In practice you don't have to worry much about the third criterion. Ambitious people are if anything already too conservative about it. So all you need to do is find something you have an aptitude for and great interest in.

Why, if David Velez had taken this to heart, he would probably have started some b2b software company to help PE or VC investors make better decisions, or some other b2b SaaS product to help entrepreneurs like his father better manage their businesses. But he didn't, and was very judicious about what and where to start. I call this top-down thinking.

Truth is, most entrepreneurs are terrible at picking high-potential businesses to start with. When they do, it's often by chance. They tend to pick where to work on based on path-dependency from decisions made in the past (like what college to go to, or which industries/sectors to start their careers on) or from hunches. I, for one (and I mean it as a *bad* example), started Qulture.Rocks because I had been interested in the people management practices of the 3G guys, which lead me to write a book about them, which led me to try to code in software what they did, and the rest is history. Most of my fellow YC batch mates similarly founded their companies out of random paths, with very little consideration to top-down thinking.

Now, is top-down thinking alone enough? Of course not. But it is INCREDIBLY important.

So what does a good product/market combination look like out there?

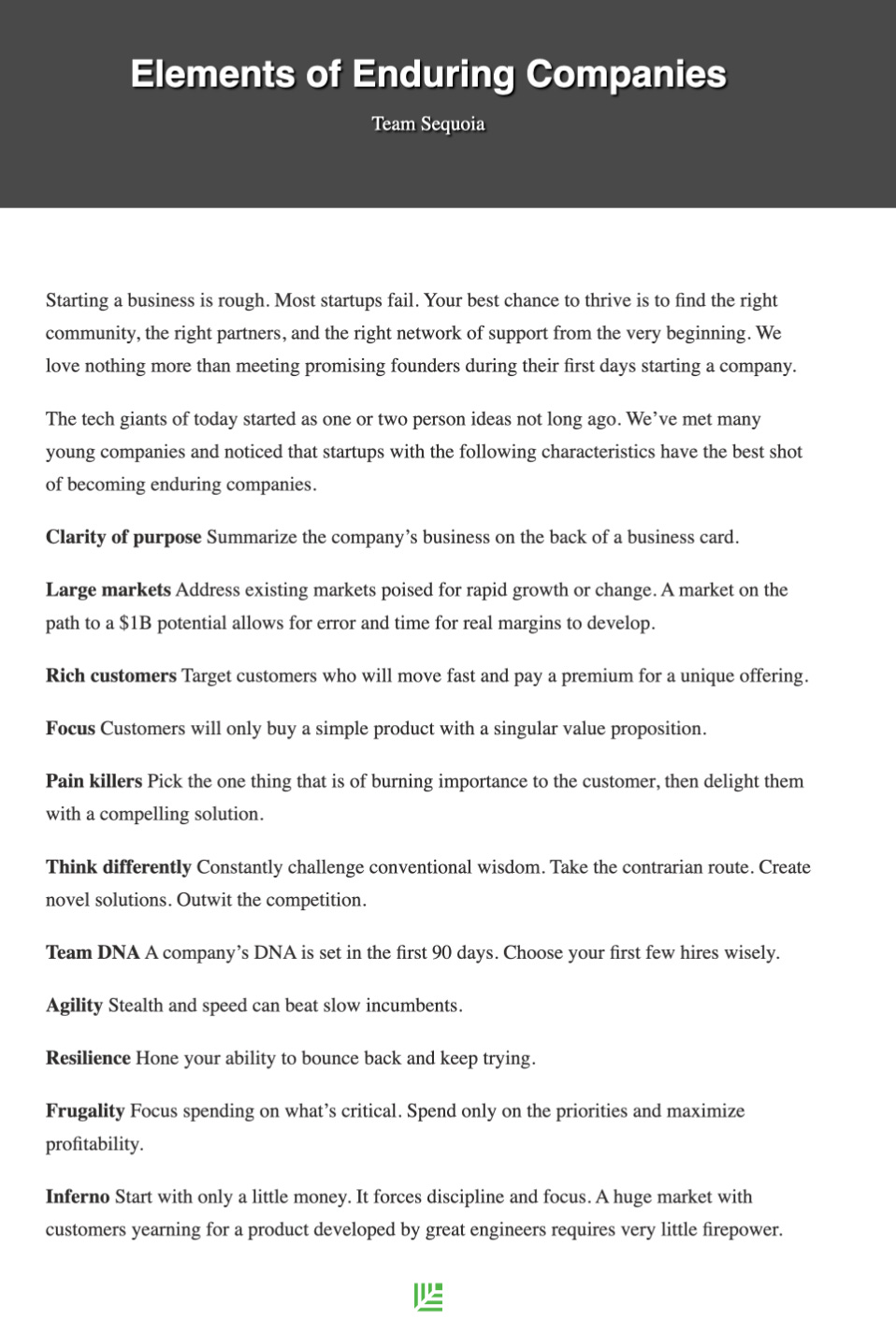

Sequoia Capital has this little-known web page I first came in contact with circa 2012 called Elements of Enduring Companies. Here's a screenshot, bc god knows if they'll delete it any day.

Let's build a list of traits for markets/products that can produce era-defining companies:

Large market of customers

who have strong, frequent pain

Large market is the first and foremost. First, we can broadly define a market as a collection of customers who have a similar job to be done. A large market, per that definition, is one where there are a lot of customers (lots of people, lots of companies) with a similar job to be done your startup is going to solve.

But lots of customers aren't enough. The job to be done you are going to solve has to be the source of lots of pain, and that pain has to be frequent. Solving once-in-a-lifetime intense pain is nice, but solving frequently-experienced intense pain is much better.

This is still not enough.

The customers in this market have to ideally have money to spend on your solution. I recently heard an interview with the founder of Duolingo. He was talking about how Android app users make up the vast majority of their user base, but iOS app users make up the vast majority of their revenue. That's because Apple phone owners are richer, have more money to spend, and spend more money. In b2b, selling to the CFO (rich, bc is the owner of the budget) is better than selling to the analyst (poor, bc has no budget at all). Selling to the CFO (rich) is better than selling to the CHRO (poor, for many reasons that are not the scope of this rant).

We looked a lot at the demand side of the market question, but the supply side of the market question is also super important. (From the demand side, a market is a collection of customers with similar jobs to be done. From the supply side, a market is a collection of companies trying to solve these jobs to be done.) There are markets where all the conditions above are true, but companies in it are still not Apples or Amazons or Googles or even Nubanks, for that matter. Airlines are the prototypical example. Bc of many factors, all profits in the airline industries get, to use Michael Porter's words, competed away. The best framework to analyze a market from the supply-side is the Five Forces Model, from Porter. The stronger the forces acting upon companies in a market, the less profitable they tend to be. The forces are the bargaining power of suppliers, the bargaining power of customers, the intensity of rivalry amongst competitors, the threat of new entrants and the threat of substitute products. I won't get in depth about each, you should read it up, but in the airlines market, some of these forces are so strong that profits are erased and everybody loses money.

So our list is, I think, now complete:

On the demand side:

large market

with rich customers

facing intense, frequent pain

On the supply side:

favorable competitive dynamics (as articulated by the 5 Forces)

There are other angles we could explore, but I think these are already plenty.